Mildred Banks was a widow in her late eighties with a net worth of about $25 million. She was facing millions in estate taxes when she finally eternally “relocated” and passed her assets on to her children. All five of Mildred’s children were already independently wealthy and did not need or even really want any of her wealth as an inheritance. Her personal lifestyle was easily maintained from $5 million of her wealth. The other $20 million was just continuing to grow, making her future estate tax problem even worse.

Since none of the children were interested in any inheritance from her, the family discussed the possibility of trying to skip them and pass these assets on to the grandchildren. But with the combined estate and generation skipping taxes (GST) that would be owed, about 75% of her assets would end up with the IRS and never make it to her grandkids. That was not an acceptable option for the Banks family.

The Banks were all followers of Jesus with a strong personal interest and involvement in supporting many different ministry efforts. They liked the idea of using some portion of this unneeded wealth to support the Kingdom causes their families cared about. Here was the dilemma. If Mildred gave these assets to the grandchildren, very little would actually get to them and nothing would go to support Kingdom causes. If she gave these assets all away to ministries the family cared about, it would eliminate all the transfer taxes, but then her family would receive nothing from her as an inheritance, which she was not enthused about either. They really wanted to do both, but no one knew how.

Over many years of working with wealthy families, I learned that there is always a way to “get there” with creative planning. This is how the Banks achieved both of their planning objectives: getting money to the Kingdom of God and getting money to the grandchildren. The strategy below was the same for all five families. (The technical memoranda included are for those of you who like to know the details.) Here is the oldest son Jim’s plan flowchart and text.

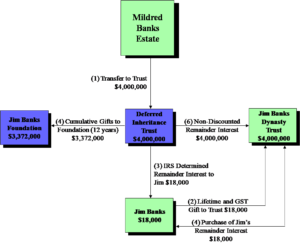

The Mildred/Jim Banks Family Inheritance Strategy

What Mildred Will Do Immediately

- Mildred will contribute $4,000,000 of her family limited partnership (FLP) shares to the Jim Banks deferred inheritance trust.

Technical Memorandum:

The deferred inheritance trust (DIT) is referred to as a charitable lead annuity trust (CLAT) by the IRS. A CLAT is required to make fixed annual payments to a non-profit organization for a specific term of years, after which the remainder will be transferred to the heir(s). The gift and estate tax laws offer a deduction for the actuarial value of the leading charitable interest in the trust. Thus, the person who creates a CLAT will be deemed to have made a taxable gift or bequest equal only to the value of the remainder interest which passes to the non-charitable beneficiaries after the charitable lead interest terminates. In this proposed plan, the current value of the future gift to the heirs is only $18,000, which will be offset using Mildred’s testamentary estate and gift tax exclusion.

Technical Memorandum:

The use of an FLP will allow the term of the trust to be shortened considerably. The gross value of the assets will be $4,000,000. However, using the recently-completed certified valuation, a discount rate of 37.7% for lack of marketability and control of the minority FLP interests reduces the amount of the gift to the CLAT to $2,509,000. Based upon the historic 7% annual rate of return generated by the underlying investments, and with the 37.7% valuation discount and the current 7520 rate (5.0%), the CLAT payout can be set at 11.2%. This payout rate considerably shortens the term of the CLAT to 12 years.

- Jim will also make an $18,000 gift to a newly-created family dynasty trust using his lifetime and generations skipping exclusion, so no tax will be due on the gift.

- The deferred inheritance trust has been designed to leave an $18,000 remainder interest to Jim. This remainder interest will be a taxable gift and will require Mildred to use $18,000 of her lifetime exclusion when making the transfer of the $4,000,000 into the DIT. Doing so avoids any estate tax on this gift.

- Once both the dynasty trust and the deferred inheritance trust have been funded, the trustee of the dynasty trust will approach Jim to buy his remainder interest in the deferred inheritance trust. Since the remainder interest of a DIT is considered a capital asset, it can be bought and sold like any other capital asset. And since the IRS and Congress are the ones who created the tables to mathematically determine what the remainder value of the trust is, there can be little dispute as to whether this will be a fair market value transaction.

Technical memorandum:

A dynasty trust, also known as a generation skipping trust (GST), provides for assets to remain in trust for multiple future family generations with no further gift or estate taxes being levied as heirs “relocate.” Depending on the state of domicile in which the trust is established, it can continue to exist anywhere from 100 years into perpetuity.

- During the twelve-year term of the trust, a fixed 11.2% of the discounted value of the trust assets (or 7% of the full value of the trust assets) will be paid out to the Jim Banks Family Foundation. The deferred inheritance trust will receive an income tax deduction for whatever it pays out to Jim’s Foundation each year. Based upon analysis, Jim’s Foundation will receive cumulative gifts of $3,372,000 over the twelve-year life of the trust.

Technical Memorandum:

The Banks currently operate The Jim Banks Family Foundation, which is a donor-advised fund (DAF) under the tax and administrative umbrella of a 501(c)3 non-profit organization. Their foundation is, for tax purposes, considered a public charity, which eliminates all the possible problems of self-dealing if they were to try to use a private family foundation for this strategy.

Technical Memorandum to Advisors:

Assuming that the trust earns only an amount equal to the payout, the trust will pay no income taxes of any kind. In the event the trust assets do outperform the required fixed payout, it will pay income taxes on the undistributed gain, and that after-tax gain will then become part of the corpus of the trust and will be distributed gift tax free to the remainder beneficiary upon termination of the trust. Likewise, if the earnings of the underlying trust assets do not equal 7%, the trust will be required to distribute whatever principal of the trust is needed in order to meet its payment obligation to the Foundation.

- Based upon the underlying assets continuing to produce a 7% return on investment during the twelve-year period of the trust, the non-discounted value of the trust should remain $4,000,000. Upon termination of the deferred inheritance trust (12 years), the remainder of the assets will then pass to the new owners of the remainder interest, the Jim Banks Dynasty Trust.

Summary

With this proposed inheritance strategy, Mildred Banks effectively transferred $4,000,000 of assets to her grandchildren and future generations utilizing a maximum of only $18,000 of her lifetime exclusions, and only $18,000 of Jim’s lifetime and GST exclusions. In order to evaluate the effectiveness of this strategy, compare it to the traditional planning strategy of simply discounting the assets (37.7%) and immediately transferring them into a dynasty trust—paying both the estate and GST taxes up front (approximately $8.6 million), allowing the grandchildren to have access and use of their inheritance immediately instead of beginning in twelve years. The following chart contrasts the traditional inheritance strategy with the Banks’ proposed inheritance strategy.

Amazingly, using our strategy, the Banks grandchildren will collectively receive only $1 million less over the next twelve years with the proposed inheritance strategy, but at the same time will have turned an $8.6 million GST and estate tax bill into over $16.8 million of Kingdom giving. For the Banks family, this creative strategy was a no-brainer!